Client

First, the market review

Figure: LME_S copper March line chart

Source: Wenhua Finance

Figure: Shanghai copper main contract March line chart

Source: Wenhua Finance

Second, the macro economy

1. Macroeconomic environment

United States

In the fourth quarter of 2016, the US GDP was revised upwards to 2.1%.

The United States applied for unemployment benefits for the first time in the week of March 25, 258,000, expected to be 247,000

US new home sales in February were 592,000, a seven-month high

February CPI was 2.7% year-on-year, the biggest increase since March 2012

February PPI was 2.2% year-on-year, the largest increase since March 2012

China

China's official manufacturing PMI for March was 51.8, higher than expected 51.7

China official manufacturing PMI 51.6 in February, expected 51.2

China's February PPI rose 0.6% month-on-month and 7.8% year-on-year.

China's February CPI fell by 0.2% month-on-month and rose by 0.8% year-on-year;

Third, industry and price dynamics

1. Industry News

1) Chile's copper output fell in February

The Chilean government, the world's number one copper producer, said on Thursday that its copper output in February was 376,948 tons, a sharp drop of 16.7% from the same period last year and the previous month. The main factor affecting the country's February copper production is the strike activity of the Escondida copper mine, the world's largest copper mine.

2) Indonesia Freeport resumes 6 months of export

According to a senior Indonesian official, the negotiations between the Indonesian government and Freeport McMulland have reached a short-term consensus. Indonesia will allow Freeport to resume operations and exports for a period of six months. Since January, the export of the Grasberg copper mine in Papua has been suspended and the two sides have been working hard to find a solution to the dispute. The new rules require that Freeport's return to exports be based on the need to convert its work contracts into special mining permits, build smelters and increase local investors.

3) SPT cuts domestic second-quarter processing fee

China's Copper Materials Joint Negotiation Group (ChinaSmeltersPurchaseTeam, CSPT) has agreed to cut copper processing refining fees by 11% in the second quarter, so the production of the world's two major copper mines has been blocked, resulting in a decline in global raw material supply. According to sources, the China Copper Raw Materials Joint Negotiation Group has set the second quarter copper processing refining fee (TR/RCS) at $80 per ton and 8 cents per pound, down from $90 per ton in the first quarter and $9 per pound. Minute.

4) Chile Antofagasta expects copper prices to rise further

Chilean copper miner Antofagasta said on Tuesday (March 14) that its 2016 full-year profit jumped 79% and said copper prices are expected to continue to rise this year. Copper prices rose more than 17% last year. Antofagasta expects that there will be a small shortage of copper supply this year, so copper prices are unlikely to return to the 2016 low.

2, the spot trend

On March 31, Shanghai Electrolytic Copper spot on the current month contract posted a discount of 150 yuan / ton - discount 90 yuan / ton, flat water copper transaction price 47230 yuan / ton - 47360 yuan / ton, premium copper transaction price 47260 yuan / ton -47390 Yuan / ton. The Shanghai period copper is narrowly arranged. On the last trading day of the end of the month, the market is light, the holders have basically entered the liquidation state, the willingness to ship has decreased, and the quotation is small and firm. In order to avoid the risk before the holiday, the middlemen have few responders. A small number of downstream festival stocks increased slightly, and the characteristics at the end of the month were obvious. The market generally expects that the copper discount will be narrowed after the transaction resumes next week.

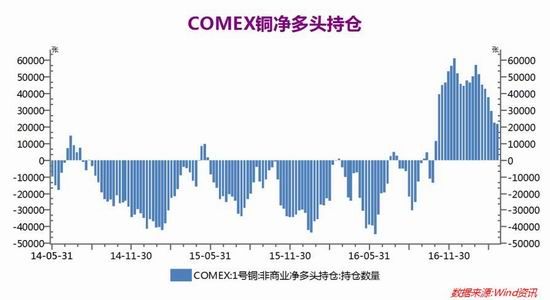

3. CFTC non-commercial positions

On the 21st of February, the net long position of COMEX copper speculation was 21670, and the bulls slightly reduced their positions.

Fourth, market supply and demand

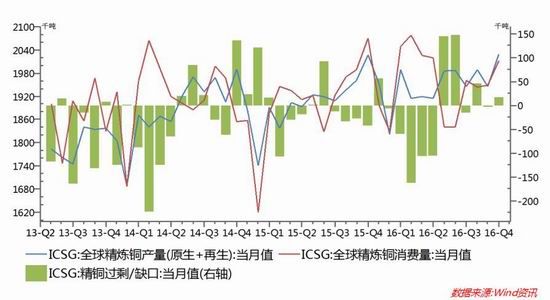

1. Analysis of copper supply

The International Copper Research Group (ICSG) released a monthly report on Monday (March 20) that the global copper market had a surplus of 17,000 tons in December 2016 and a supply shortage of 55,000 tons for the whole year, much lower than the full supply shortage of 164,000 in 2015. Ton. According to ICSG data, the mine output in December was 1.771 million tons, the global mine production capacity reached 2.035 million tons, and the mine capacity utilization rate was 87.0%. In December last year, global refined copper production was 2.029 million tons, and refined copper stocks were 1.395 million tons.

2. Analysis of domestic copper demand

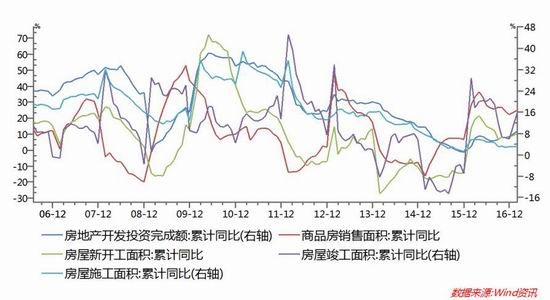

Real estate industry: Last year, the effect of regulation and control began to show, and the hotspot city property market gradually returned to rationality, but the third- and fourth-tier cities were affected by the spillover effects of first- and second-tier hotspot cities, and sales were hot. On March 17, hotspots in the first and second tier cities re-enforced measures to restrict purchases, and some third-tier cities gradually introduced restrictions on purchases. It is expected to only suppress excessive rapid growth in the housing market. In January-February 2017, the national real estate development investment was 985.4 billion yuan, a nominal increase of 8.9% year-on-year, and the growth rate was 2 percentage points higher than last year. The construction area of ​​real estate development enterprises nationwide was 622.95 million square meters, an increase of 3.2% year-on-year, and the growth rate was the same as last year. The completed area of ​​housing was 161.41 million square meters, up 15.8%, and the growth rate was increased by 9.7 percentage points; the sales area of ​​commercial housing was 140.54 million square meters, up 25.1% year-on-year, and the growth rate was 2.6 percentage points higher than that of last year. The data shows that the new round of real estate market regulation and control measures adopted by local conditions and sub-city measures are correct, and the results are obvious. From the situation in January and February, the process of destocking in the third- and fourth-tier cities is accelerating.

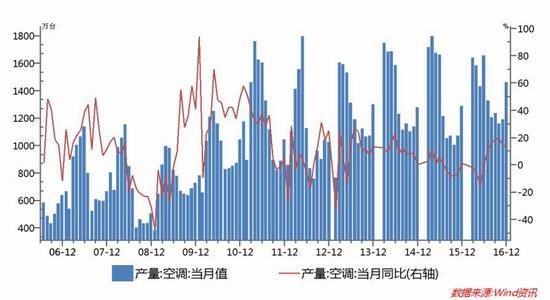

Air-conditioning industry: In December 16th, the output of air-conditioners was 14.62 million units, an increase of 13% year-on-year. The growth rate of domestic air-conditioning domestic sales reached a new high, and air-conditioning was perfect in 16 years. In the same month, the growth rate of domestic air-conditioner shipments reached a new high in the past eight years. Considering that the domestic sales volume in the same period of 2015 was reduced to a very low level by the channel destocking, the monthly growth rate continued to rise sharply. Product price increase expectations and real estate lags drive demand recovery is also an important factor for the industry's domestic sales performance continues to be eye-catching; in general, the 16-year air-conditioning industry experienced a cliff-like decline in the channel inventory in the first half of the year, with inventory declining in the second half of the year After the completion and hot summer air, the “V†type reversal was realized, and finally the domestic sales only declined slightly in the whole year; as the channel destocking period came to an end, the industry's subsequent return to growth was more worth looking forward to.

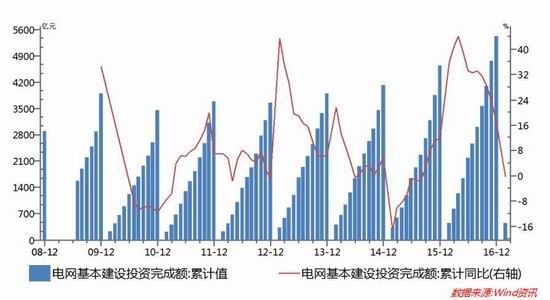

Grid investment: The cumulative year-on-year growth rate of power grid infrastructure investment in January-February 2017 decreased by 0.3% compared with the previous period, mainly due to the high base last year. The growth rate of power grid investment this year will mainly come from the construction of UHV and the transformation of rural power grid. The UHV's consumption of copper is relatively low. The provinces covered by Shaanxi, Anhui, Chongqing, Tibet and the southern power grid are the focus of rural power grid reconstruction. However, the scale is no longer the same as in previous years, and the increase in copper consumption will be reduced. It is expected that this year's grid investment will continue to maintain investment last year, supporting copper prices.

V. Outlook for the market outlook

First of all, on the macro side, the US dollar fell first this month. The main reason was that the Trump medical reform vote was delayed. The market questioned Trump’s ability to implement the New Deal. The US dollar once weakened, and the recently released domestic economic data was bright. The Fed chairman uttered a hawkish, the dollar rose in the short term, but it is expected to suppress the copper price. .

Domestically, in the short term, as the central bank's MPA assessment ends at the end of the month, the money market and liquidity are generally loose. Domestic PPI and CPI continued to remain high in February, and this year's high probability will maintain moderate warm inflation, which is good for commodities.

Secondly, from a fundamental point of view, the strikes in the Chilean and Peruvian mines have had a contraction effect on the supply side, and Chile's copper mine output in February fell sharply year-on-year. Therefore, although the strike in Chile ended, the supply side still has a lot of copper prices. On the demand side, the housing market unexpectedly hot in January-February, far exceeding market expectations, is expected to benefit copper demand. Overall, although the housing market is subject to a limited purchase policy, it is expected to be relatively stable in 2017, and it is difficult to collapse. In addition, China will invest 3.34 trillion yuan in the power grid during the 13th Five-Year Plan period. Speed ​​up. The market is still expecting good demand for copper.

In terms of inventory, the stocks of the two cities gradually stopped falling and supported this month, supporting copper prices. Overall, global inventories are still in the vicinity of historical averages, not too high. Shanghai copper is expected to be strong in April. Focus on the progress of the remaining copper mine strikes. for reference only.

Guangzhou Futures

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Microfiber Towel,Microfiber Printed Towel,Microfiber Drying Towels,Quick Dry Microfiber Towel

Wujiang Rongchao Silk Co., Ltd , https://www.wujiangrongchao.com