This article was first published on WeChat public account: RMB transactions and research. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Since the beginning of this year, the impact of changes in liquidity conditions on the market has continued to increase. From a longer-term perspective, as the liquidity channel for foreign exchange accounts is increasingly exhausted, the central bank's monetary policy has gradually become the main channel for liquidity. Monetary policy has the advantages of clear policy intentions and proactive and controllable advantages. However, at the same time, excessive dependence on monetary policy will also face some constraints, such as insufficient collateral and narrow scope of delivery.

Therefore, while paying attention to the amount of liquidity, it is also necessary to consider the mechanism similarities and differences between the various channels of liquidity, such as the same amount of liquidity, but the channel may have different impacts on the market.

To this end, we systematically sorted out the four main channels of liquidity: fiscal, cash, foreign exchange and monetary policy, and compared them. On this basis, this paper will focus on the relationship between fiscal release and monetary policy, and the effect difference, and finally deduct and judge the future liquidity environment.

The central bank announced today that “the fiscal expenditures at the end of the month have increased, and the liquidity of the banking system after the central bank’s reverse repurchase expires is at a relatively high level. On June 26, no open market operations will be carried outâ€. Following the second consecutive working day of the central bank's suspension of open market operations since last Friday, there is a view that the central bank's move may mean that the market environment with relatively loose market liquidity is coming to an end, and the market will once again face a tighter funding situation.

However, we believe that this is only a normal monetary policy adopted by the central bank in accordance with established practice at a specific time node, without excessive interpretation. And the basic currency is put into the market through fiscal expenditure, which can improve the liquidity level of the whole market compared with monetary policy tools. For the bond market, the liquidity level of the market is still relatively abundant in the near future. We insist on the judgment that the top center of the 10-year government bond yield is 3.6%.

Currently, the bank has four means of obtaining the base currency.

At present, there are four main means for banks to obtain the base currency:

cash

Monetary policy tool

Financial expenditure

Foreign exchange

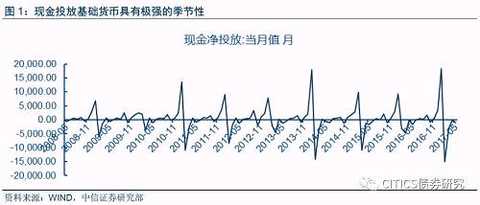

For cash, getting the base currency through cash is extremely seasonal. In general, the central bank will conduct cash placement for the cash needs of residents at special time points. Especially in the Spring Festival, National Day and other festivals, the central bank will put a large amount of cash to ensure that the residents have sufficient cash during the holiday season. After spending these hours, the central bank will gradually withdraw cash and recover this part of the liquidity.

|

The central bank's monetary policy tools mainly include reverse repurchase, MLF, SLF, SLO, PSL, treasury cash deposits, and central bank bills. Currently, there are reverse repurchases (including 7 days, 14 days, and 28 days), MLF (currently 6 months and 12 months), and PSL (for policy banks, which are used for shantytown renovation and other currencies). Sexual expenditure). The amount of base money put by the central bank through monetary policy tools is related to the market interest rate level and liquidity status. If the inter-bank liquidity pressure increases at the end of the quarter, it will increase the amount of funds and ensure sufficient funds in the banking system. After spending a lot of liquidity, such as spending, it will reduce delivery.

At the same time, it should be noted that monetary policy tools are not targeted at all banks. According to the list of the first-tier dealers of the open market business announced by the People's Bank of China, the main target banks of the central bank's open market operations are the five major banks of China Agricultural Construction, the Postal Savings Bank, some large joint-stock commercial banks, a small number of city commercial banks, rural commercial banks and individual foreign banks. Brokers; the central bank mentioned in the first quarter of this year's monetary policy report that the medium-term lending facility (MLF) operating bank is the main bank with better macro-prudential assessment (MPA) compliance among the primary traders in the open market business.

Fiscal expenditure is another means of placing the base currency. By redistributing fiscal revenue, the central government will put the funds of the central bank to the local government, and the local government will invest the funds into the real economy through public expenditure, which will realize the transfer of funds from the central bank to the commercial banking system.

The amount of financial expenditures is mainly determined by the government's fiscal plan and the domestic macroeconomic situation. Generally speaking, different macroeconomic development targets correspond to different financial plans, and actual and expected economic changes will also be made to the government. Fiscal expenditures have an impact and unplanned expenditures may occur.

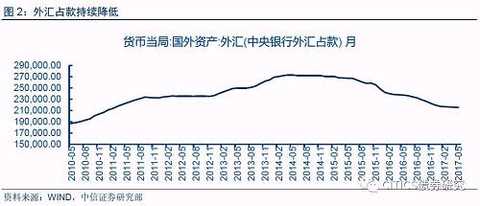

In addition, foreign exchange is a means of base money that China relies heavily on before 2015. The logic of releasing liquidity through foreign exchange is to invest large amounts of money for foreign exchange exchanges. It requires the state to purchase foreign exchange in its own currency, thus increasing the “money supply†and thus forming foreign exchange. The amount of foreign exchange is mainly determined by the exchange rate level and the balance of payments. The international macroeconomic situation, domestic and international spreads, etc. determine the demand for foreign exchange, which in turn determines the number and trends of foreign exchange holdings.

Fiscal expenditure is one of the basic currency instruments and has more audiences.

Among the means of placing the base currency mentioned above, the base currency placed through fiscal expenditure has a wider audience than the other two.

As we all know, banks that are qualified to obtain the base currency directly from the central bank through monetary policy tools are generally larger and better qualified banks, and many rural commercial banks and city commercial banks cannot obtain funds through this channel. As highlighted in our previous report, the imbalance in the structure of monetary policy instruments is a major factor in the current market liquidity. Large banks are eligible to obtain low-cost funds directly from the central bank through OMO/MLF, and liquidity is relatively abundant; and most local small banks, including most local city commercial banks, rural commercial banks, rural credit cooperatives, etc., cannot directly go from the central bank. Obtaining funds, and at the same time facing the problem of a significant decline in deposit growth, it is facing greater liquidity pressure.

As the other main means for the central bank to put the base currency, foreign exchange has been gradually decreasing since the beginning of 2015. Although the decline has begun to narrow in the near future, and there are signs of recovery as the international economic situation improves, small and medium-sized banks do not have a large amount of foreign exchange reserves for trading with the central bank. Therefore, even if foreign exchange accounts start to increase, there is still no small bank. Get the opportunity to launch the base currency.

|

As an important means of placing the base currency, fiscal expenditure is one of the important channels for small and medium-sized banks to obtain the base currency. Local government financial funds are used for public services such as local infrastructure. These currencies enter the real economy through the banking system, and some of the funds will flow to local small and medium banks after the funds are obtained. In this way, its liquidity situation will be improved.

The base currency obtained through fiscal expenditure or more helpful to the volatility of funds

The main way to guide the funds out of the market in the early stage is to control the scale of inter-bank interbank business through regulatory means, reduce the idling of funds within the banking system, and promote the transfer of funds to the real economy. This approach has achieved certain results, and the growth rate of M2 in May has declined. To a certain extent, the situation of idling funds has been suppressed.

However, this also led to the fermenting of panic in the interbank market in the early stage. Some banks have reduced the capital outflow due to the pressure on the capital, and the cost of capital in the interbank market has soared. Small and medium-sized banks that rely on inter-bank certificates of deposit and inter-bank dismantling to obtain funds have taken huge financial pressures. The rise in capital costs has begun to shift to the real economy, resulting in passive pressure on the real economy.

And by means of financial expenditures, the funds can be directly invested in the real economy.

On the one hand, local banks that are the source of direct financing for “agriculture, rural areas and farmers†and small and micro enterprises can support the development of their credit business and inject blood into the real economy;

On the other hand, the government can directly provide funds to related enterprises through investment in public services and infrastructure, which can promote its development.

Through the cooperation of fiscal policy and monetary policy, the problem of imbalance in the liquidity structure of monetary policy tools is adjusted. While ensuring the stability of the liquidity of the banking system, capital is injected into the real economy to ensure its smooth operation, which can promote the detachment of funds. It also reduced the impact of using regulatory means to force de-leverage on the financial system, preventing passive pressure on the real economy, and maintaining the general stability of finance and entities.

Suspension of open market operations or policy practices at the end of the quarter will not exacerbate funding constraints

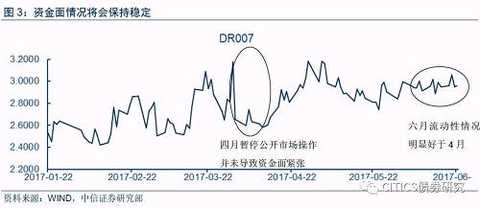

The suspension of open market operations at the end of the quarter was not the first of its kind. At the end of March, the central bank suspended its open market business for more than 20 days for the same reason, but the funds did not fluctuate greatly. On the one hand, at the end of the special time at the end of the season, the MPA and LCR assessments were smooth, and the large and medium-sized banks began to borrow funds from the outside, while the demand for funds in the inter-season began to decrease. The relationship between supply and demand determined that the funds were loose.

Taking the 7-day interbank pledged repo rate (DR007) as an example, during the ten days from March 24 to April 12 when the central bank suspended the open market manipulation, interest rates continued to fall, from the March 31 high. 3.17% gradually fell back to a phased low of 2.59 on April 12.

According to the DR007 monitoring interval mentioned in the central bank's monetary policy report in the first quarter, it can be judged that the liquidity level in this period is in line with the central bank's regulatory standards, so the suspension operation has not produced a huge amount of funds. Shock. After that, DR007 continued to rise because of the panic caused by the CBRC's frequent regulatory documents in the industry, and it has nothing to do with central bank policy.

|

At present, the central bank’s monetary policy is “not loose and tightâ€, which has been alleviated compared with the previous “stable neutralityâ€. While standing at a similar time to March, we believe that the central bank will protect the funds in accordance with its regulatory indicators and continue to moderately de-leverage while ensuring sufficient liquidity to guide the funds out of the real world. If the supervision is no longer overweight, the capital fabric will not be in a tight situation in late April.

Bond market strategy

The central bank once again suspended its open market operations today, due to the increase in fiscal expenditures and the abundant liquidity of banks. We don't think this situation needs to be over-interpreted.

On the one hand, the combination of monetary policy and fiscal policy can balance the volatility of funds and maintain liquidity stability.

On the other hand, it can also reduce the lack of structural imbalances in monetary policy instruments.

Suspending public operations does not mean that liquidity is tightened, just a customary operation at a particular point in time. For the bond market, there is no need to over-interpret the current operation of the central bank, and the recent funding will remain stable. We still insist that the 10-year bond yield range is unchanged at 3.2-3.6% (end).

The product has passed the Global Recycled Standard (GRS) certification, which is in line with the global green and environmental protection trends, and can help to enhance market competitiveness of "green" and "environmental protection" as an "environmental friendly enterprise".

The product specifications cover from 20D to 1120D, the content of recycled materials is from 20% to 100% generally and it can be customized , no difference in performance from conventional products.

Recycled Spandex,Spandex Coated Wire,Recycled Nylon Spandex Fabric,Stretch Recycled Nylon Spandex

Huafon Chemical Co., Ltd. , https://www.qianxispandex-intl.com